Capitalizing on aligned interests with banks to diversify re...

Discover an innovative case study on how a European insurer utilized fund structures to meet banks' liquidity needs, enhancing returns under Solvency...

In an environment characterised by interest rate volatility and episodic market stress, institutional investors increasingly seek solutions that enhance cash returns without compromising liquidity and capital preservation.

Our Smart Return Solutions are designed to capture a structural premium embedded in the bank funding market, a premium that is typically inaccessible through traditional treasury instruments such as cash and term deposits, while maintaining conservative risk parameters and high operational standards.

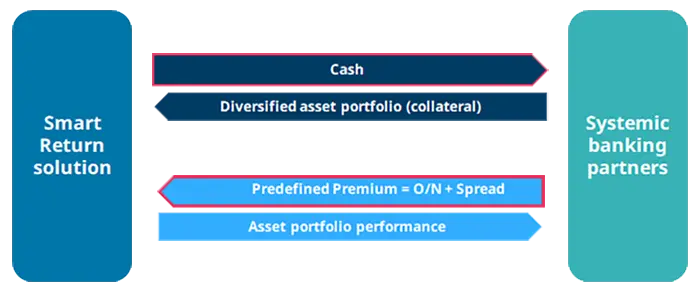

Our strategy uses a dual-transaction structure with systemic banks seeking alternative sources of funding, enabling predictable returns within a controlled counterparty framework.

Our vehicle buys a diversified pool of assets from the bank

The bank pays the vehicle a premium over the overnight rate (fixed upfront) in exchange for the assets' performance

Source: Amundi

Further details on the performance, investment process and structuring framework are available upon request and tailored to your needs.

AUM in Smart Return Solutions1

Track record delivering Smart Return solutions1

dedicated Portfolio Managers specialised in banking solutions

Smart Return solutions are designed to provide targeted, capital-efficient tools to help you navigate evolving market conditions.

Where can these solutions add value:

1.Amundi, as of 31/03/2026

A range of investment strategies combining ownership of asset baskets with fully collateralised Total Return Swaps (TRS) to deliver a money‑market‑style return (OIS + spread) with daily liquidity. The strategy is available through multiple investment vehicles, including commingled funds, dedicated funds and segregated mandates.

The vehicle purchases a basket of assets and uses a TRS with bank counterparties, so it receives Overnight Index Swap (OIS) plus a spread, while the counterparties receive the performance of the asset basket.

Economically no — the TRS neutralises equity performance so net equity exposure is close to zero; residual risk relates to counterparties and collateral.

A selected panel of investment banks. Exact counterparties and spreads differ by sub‑fund and are available on request.

Contracts include margining and collateral monetisation procedures; the manager may liquidate collateral and portfolio assets as required. Full details are set out in the contractual documents.

The solutions are not marketed as cash equivalents, though some investors may obtain such treatment from their auditors. Accounting classification depends on the investor’s rules.