Summary

Highlights

The crisis will likely accelerate Europe’s shift to strategic autonomy and greener energy to reduce geopolitical risk.

With inflation risk on the rise, central banks will likely become more cautious and embrace a wait-and-see approach.

The need to stay vigilant and well-diversified is high, and investors should look beyond the crisis for areas of quality through careful selection.

In this edition

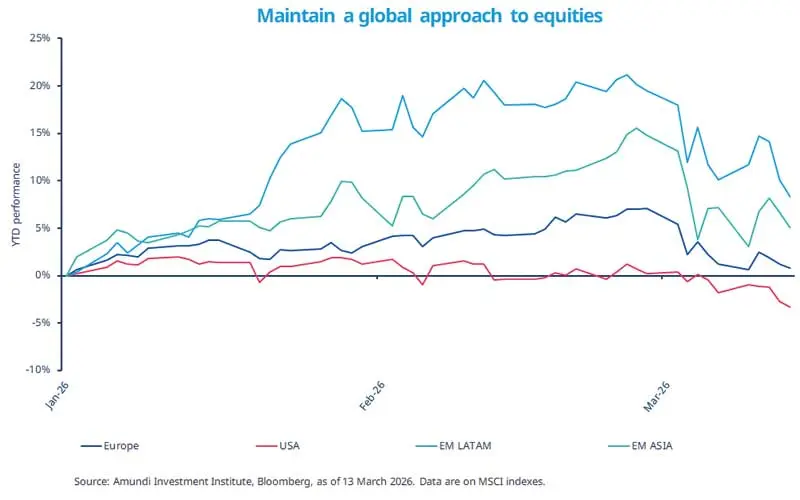

The impact of the Middle East crisis on equities across regions reflects economies’ sensitivity to higher energy prices and renewed concerns about inflation. In some cases, it represents a pull‑back in markets that have performed strongly this year. While US assets (including the dollar) have been more resilient during this episode, vulnerabilities associated with expensive AI segments and a large US fiscal deficit remain. In contrast, EM Asia and European markets declined sharply, given those regions’ dependence on energy imports. Despite this volatility, these markets have outperformed year‑to‑date, and LatAm has been a top performer.

These movements affirm the need to maintain a global diversified stance across both developed and emerging markets, as it provides multiple layers of resilience for long-term returns. A key factor is the scale and the duration of disruption in the Strait of Hormuz.

Key dates

Germany ZEW, China Industrial Production and Retail Sales |

FED interest rates decision, USA PPI index, EA CPI, South Africa CPI |

ECB rate decision, Japan Industrial Production |

Read more