In a nutshell

The credit markets' reaction to the conflict in the Middle East was very short-lived. With the announcement of the fragile ceasefire, credit spreads erased most of their subsequent widening, despite the persistence of geopolitical uncertainties. Valuation levels do not reflect major concerns about global growth. For now, investors view the impact of the conflict as a temporary inflationary shock with limited effects on growth. Wholesale oil and gas prices have risen by roughly 60% and 70% respectively. Government bond yields have increased across the curve, particularly at the short end. Rate markets have repriced inflation risks and expect less-accommodative central banks, but investors have not substantially revised their growth risk assessment.

We expect the impact of the shock on inflation and growth to remain moderate and temporary. The conflict in the Middle East represents a supply shock to our economies, a shock that generates higher inflation, lower growth, and a high level of uncertainty regarding the extent of its impact. The longer this conflict lasts, the more it will cost us in terms of growth. Our central scenario foresees a near resolution of the conflict.

Euro Area: Headline inflation is expected to average 2.8% in 2026, then return to around 2.2% in 2027. The moderate pass-through of energy price increases to the rest of the economy should allow the ECB to maintain a status-quo stance. Economic growth is expected to maintain a steady policy stance. 0.8% in 2026, then pick up to 1.1% in 2027.

US: Headline inflation is expected to average 3.3% in 2026, then decline to around 2.4% in 2027. We maintain a Fed rate cut in 2027.Economic growth is expected to average 2.3% in 2026, then ease to 2.0% in 2027.

We expect central banks to keep rates on hold in 2026.

A central question for investors is the reaction function of central banks: can this energy shock be considered temporary or does it require further tightening? To answer this, central banks will examine three variables:

(i) The duration and intensity of the shock to energy price

(ii) Second round and indirect effects i.e., the transmission of energy price increases to other sectors of the economy. The risk is that a temporary rise in energy prices turns into self-sustaining and more generalized inflation. Christine Lagarde has explained that the ECB will monitor commodity markets, potential supply bottlenecks, firms’ selling-price expectations, demand indicators, and wage indicators

(iii) The anchoring of long-term expectations. A de-anchoring of inflation expectations complicates economic agents’ planning and poses financial stability risks.

We see the risk of a second-round effect to be less important than in 2022. The post-Covid period was characterized by strong demand driven by accumulated savings and tight labour markets. On the contrary in 2025, US. job creation was among the weakest since the early 2000s (outside recessions). In Europe, wage pressures and hiring remain also much lower compared with 2022. Moreover, interest rates are higher than before the start of the war in Ukraine. At the beginning of 2022, the ECB still had its deposit rate in negative territory.

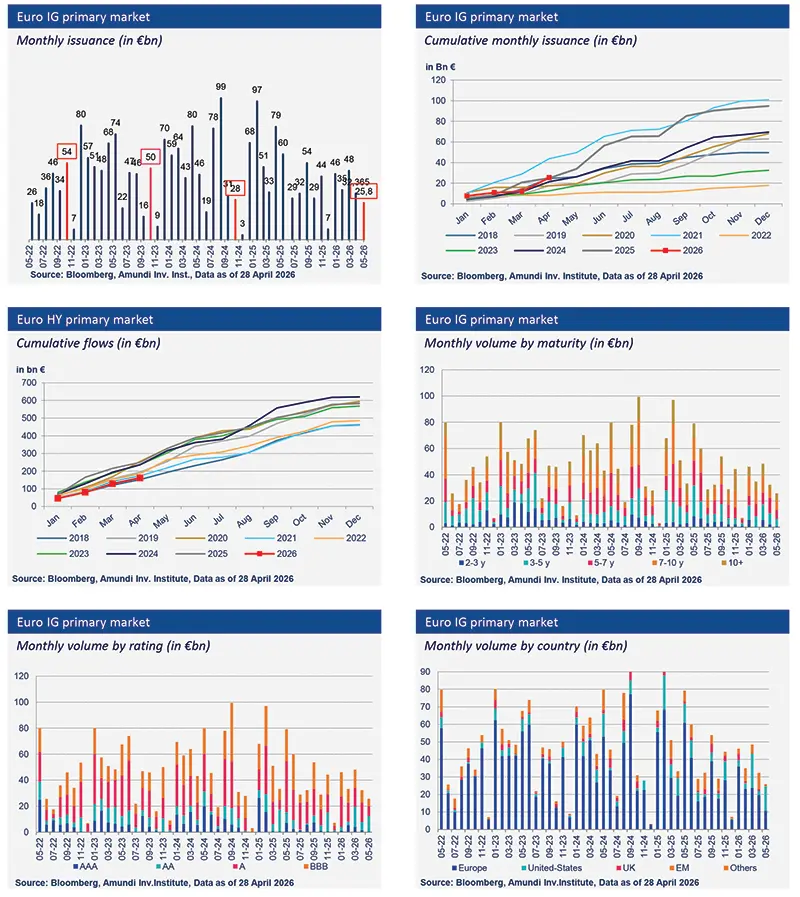

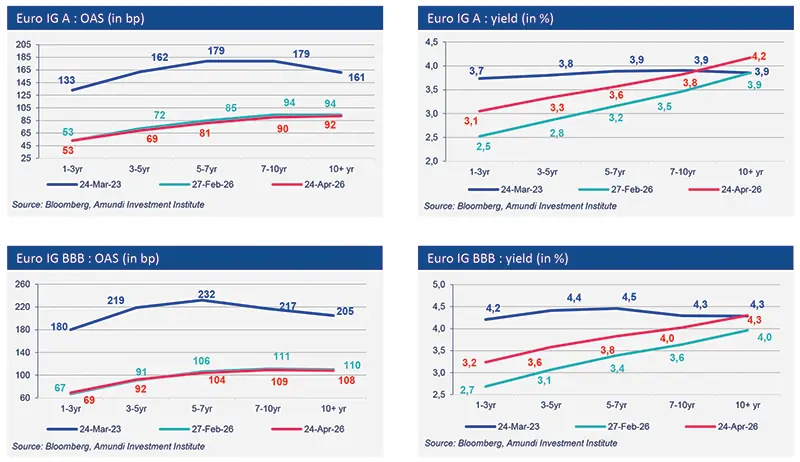

The resilience of credit markets is explained by corporate solid fundamentals. US. and European corporates have managed their balance sheets very prudently since the health crisis. They took advantage of the post-pandemic period of ultra-low rates and economic recovery to improve their credit profiles. In recent quarters, corporates to strengthen the from a very active primary market and strong investor demand, particularly in the Investment Grade segment, attracted by attractive yields. Thus, issuers have been able to refinance their debt easily. There is no refinancing wall comparable to 2008.

The resilience is also explained by one dominant factor: sustained and significant investment flows into this asset class. Rising interest rates attracted yield-seeking investors, providing strong technical support for euro-denominated investment-grade credit. Demand consistently outstripped supply, creating a dynamic where investors continue to "buy dips”.

Our view on Investment Grade credit remains constructive in the context of our central scenario, which still envisages a moderate slowdown in growth and prudent central banks. However, a more pessimistic scenario is possible. If the straits of Hormuz remain largely closed through the summer, oil could rise durably above $100 barrel. A deterioration of the economic environment with a protracted conflict combined with a tightening of financing conditions would lead us to adopt a more cautious overall view on the asset class.

Primary market Investment Grade

Market data

Find out about our treasury offer